Welcome to Stall St - 1st week recap

Welcome to Stall St - 1st week recap

A week in review

Wow, what a start! Happy weekend and welcome to Stall Street - many thanks for subscribing and reading. Over the last few days, after posting some work and research on Twitter, receiving over 500 views on the Carvana research, and taking a comment beating on Seeking Alpha, I’d like to take a moment to recap and share forward focus.

Started the week with a post on Seeking Alpha about fledgling EV startup Canoo Inc ($GOEV), which immediately got savaged in the comments – as someone whose main experience is in business operations, not insider trading, I’m ok with falling on my sword for missing that a co-founders large share sale was a result of CFIUS compliance, not a lack of confidence. Lesson learned, I’m here to advance my analysis skills and take feedback.

On the other hand…

This feels like a good time to point out that I am a defender of nuance. Extremist and dogmatic arguments benefit no one, except drug companies who treat high blood pressure. I do my level best to be impartial, analytical, and steer safely clear of emotional tripes, because that is what analysis is. Feel free to disagree with what I say, but we can all agree that dialogue is most productive when it doesn’t burst any blood vessels. Onwards!

Carvana really surprised me, digging in this week. I genuinely expected to see a “no way out” catastrophe, given their extreme debt, consistent net losses, and small cash pile. As a dealer, if Carvana started bidding against me in a lane, I just left. I watched them consistently overpay 10% or more above wholesale prices, sometimes more than my entire predicted unit GP. So, of course I’m curious how they are sustaining themselves.

My opinion was, well… maybe. Just not this year. Again, nuance. I think they are playing fast and loose with debt, are loaded with risk, and I personally would never run my corporate growth as white hot as they are. But I don’t think they are stupid - they’ve managed to avoid BK so far while compounding debt and barely improving cash. How? Their guaranteed loan purchases from Ally and growing revolving credit lines provide just enough incremental cash YoY to cover near term debt. While fundamentally it looks awful, it seems there is more gray area than this:

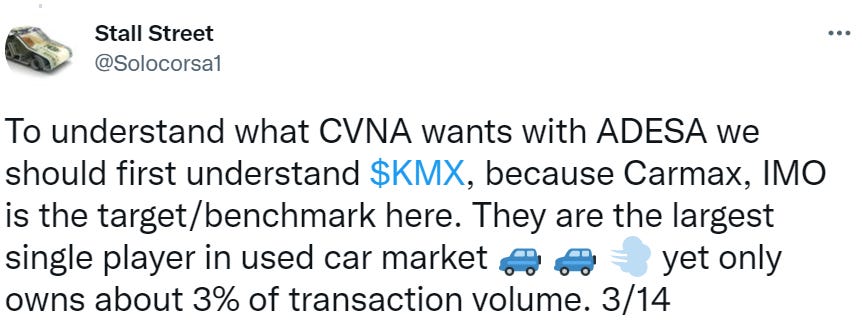

And this:

CVNA may very well fail in the future, but ignoring how they are getting by now is a disservice to their investors and their customers.

Also wrote a more in-depth Twitter thread about ADESA and what CVNA likely plans to do with their new wholesale toy.

That was most of the first week. Also feel free to check out some business assumptions on Sono Motors ($SEV) from earlier in the month.

Ok, this will be my first and last self-promotion: I started Stall Street at the beginning of March 2022 to document my financial research into public auto companies, especially pre-revenue, pre-product manufacturers. Who am I? My experience includes 12 years of strategy, operations, communications, and business development in diverse automotive environments including OEM, Wholesale, and Retail. If you like cars, you’re in good company here. I’m also a performance driving coach, occasional racer (2 wheels and 4), general motorsport nerd, and will do my very best to convince you to get behind the wheel of a proper sports car, on a proper track, and/or to watch F1 every weekend.

Speaking of racing, I can’t help but mention, F1 is racing Sunday in Saudi Arabia. And what a wild reminder it was yesterday that F1 often races in questionable locales (does that count for the new Miami race in 2022?). It seems the race will go on, however, and Ferrari is back!

Next week, the focus will be another pre-revenue EV startup that has made some very misleading claims and hides a docudrama-worthy past and cast. Looking forward to sharing.

Obligatory disclosures: My research is for my own interests and learning, and I am not an expert in financial modeling or predictions. I mostly just know a lot about cars, love research, and by nature I am extremely curious and skeptical. I receive no comp for anything I write, this is not investment advice, and all opinions are my own.