Is Carvana Headed to Bankruptcy?

I dig into their debt, including the ADESA deal, and what it means for the company.

Over the last few weeks FinTwit has been aflutter with frustrated value investors and gleeful day traders over a name I became very familiar with when I was running a dealership. That company is Carvana. Now, I did a previous take on the ADESA deal a few weeks ago, where I speculated about where the debt was coming from and how the deal might affect all those involved. Consider that a “rough take” and what follows much more thorough. I’ll address ADESA at the end, but in the meantime, everyone wants to know, how can CVNA continue operating without a cap raise? It’s been perplexing me as much as everyone else, so I finally dug in.

If you’re interested, a summary thread has been published on Twitter. You can follow me there @solocorsa1

There’s been lots of talk about how $CVNA can continue operating without a cap raise because they have minimal cash relative to expenses (±$400m) and $10 billion in debt, if you include the $3 billion ADESA deal, which closes in Q2.

Here’s how they’ll do it.

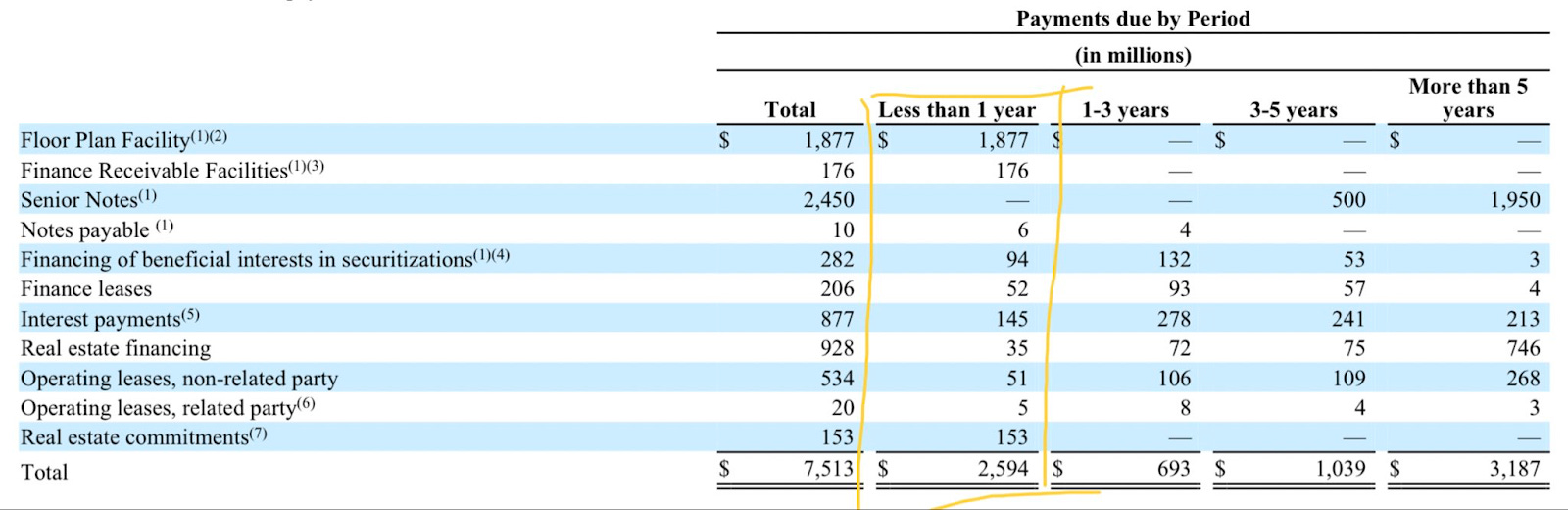

The first thing to note is that the total debt due in 2022 is around $2.6B. That’s a lot, but it’s far less than the full $10B. The bulk of these payments (~$2 billion) are interest charges for floorplan and finance receivables, and the remaining $600 million is mainly real estate based. Let’s start with the bigger chunk. Floorplan is not unique to the auto business, but it is very common and these loans are used by the majority of dealerships to purchase inventory without tying up their own capital. Typically a floorplan loan is a very short term, 90 days or less, with ballooning interest payments after that so the dealership is encouraged to sell the car quickly. The main thing to remember is that these are short-term credit facilities for inventory and interest is paid back once a vehicle is sold.

The bulk of Carvana’s cash expenditures are on inventory, reconditioning, marketing, etc. I found that most of these cash outflows are simply paid with this short term revolving debt, like floorplan financing or “Finance Receivable Facilties.” Not out of pocket, not out of Carvana’s precariously low cash position. This all makes sense; dealers prefer keep their cash free and it allows faster growth. And typically as is the case with floorplan lenders, the larger your inventory and cash position, the more they are willing to lend. And we find the same with Carvana noted below in the 10k. The bigger the balance sheet, the bigger the credit limit.

What is interesting however is this line, also paraphrased from 10k: “[Income] from financing activities was approximately $3.5 billion December 31, 2021, up from 1.2B 2020, resulting in changes in our short-term revolving facilities, along with increased net proceeds from long-term debt” (emphasis mine). Carvana has historically been known as a terribly bad car buyer that often overpays for inventory, but makes up for it with the financing. This statement really confirms their reliance on financing (as many as 80% of their units) and shows how they differentiate themselves from traditional brick and mortars.

When Carvana originates a loan as part of their sale, that loan is repackaged and sold at a premium to various loan servicers. Most dealers rely on banks or credit unions to arrange their financing, and then get a small cut for originating the loan. Carvana’s parent company DriveTime owns a loan servicer called Bridgecrest, a subprime specialist, who initially was the main servicer buying loans off Carvana’s books, but Carvana’s reckless abandon purchasing vehicles anywhere they could, no matter the cost, gave them a lot of inventory to market to people who need car loans.

Eventually they were able to make a deal with Ally Financial, one of the world’s largest auto financiers. Ally would buy more and more of Carvana’s loans as long as they met Ally’s requirements, which are known for being, let’s just say “flexible.” Carvana itself doesn’t exactly have stringent loan eligibility requirements - if you have $4,000 in annual income, are over 18, and have no bankruptcies, you’re approved. Up to a point of course. Carvana records the sale of the loan as a finance receivable and Ally pays them a premium for it.

So, I found as those balance sheet assets get bigger and bigger, they are themselves used as collateral to permit more cash draw from the $2.5 billion in “unused commitments” from their short-term lenders. This is a virtuous cycle for Carvana, because the more loans it sells to Ally, DriveTime, the more their balance sheet pumps, giving them in turn a bigger credit line to buy more cars.

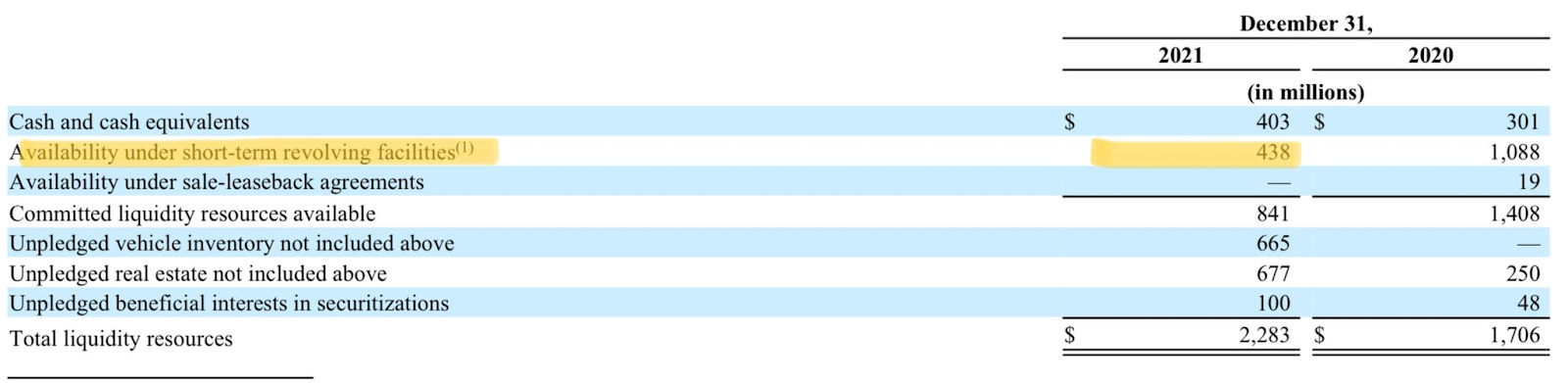

This system is what Carvana is calling “Asset-Backed Financing.” You can see right below they have $438 million of liquidity in addition to their cash from these short term credit lines… and as long as the loans are being sold, there’s ALWAYS more where that came from.

It’s really a great deal for the lenders. In fact, more and more of them are hopping on to get a piece of the Carvana inventory action. Look at all those credit lines!

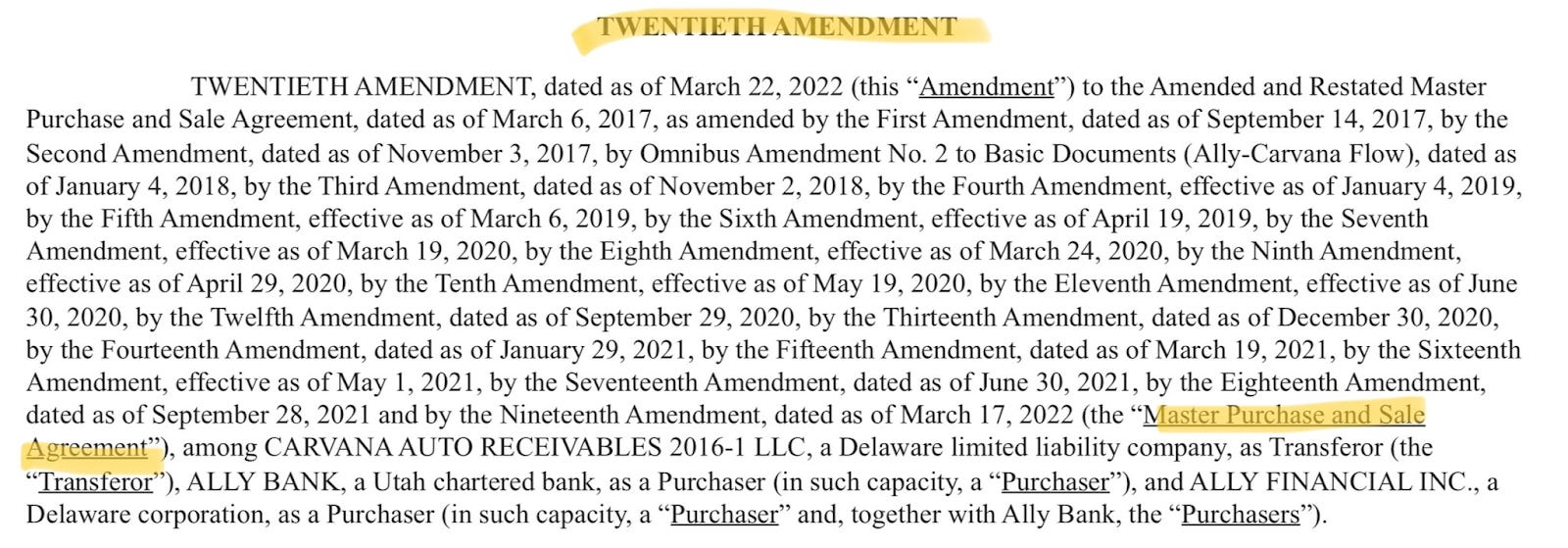

These lenders see their interest payments as secure, because unlike traditional dealers, Carvana is such a big loan originator that Ally became willing to GUARANTEE to buy an ever-increasing amount of loan paper from them (at an unknown premium). In this 8K from March 22nd, you can see they submitted their 20th (🤯) amendment increasing Ally’s commitment to purchase up to $5 BILLION. They can barely write the amendments fast enough!

Yes, DriveTime/Bridgecrest and CVNA’s own trust are also still buying loans from CVNA, which is their claimed vertical integration, but Ally is the real big fish. Essentially what we are seeing here is Ally using Carvana as one of their premier loan originators… so it makes sense that Ally would pay up for all this incoming paper.

Meanwhile, Carvana is guaranteed a fat balance sheet and loan sale income, and as we’ve noted, this in turn unlocks more cash from their floorplan companies.

Many have noted that Carvana has terrible margins on the vehicle sale. But they really don’t care that their front end GPU is bad, because they make up for it in the back half of the transaction, primarily with the loan sale and also service contracts and GAP. And it’s all guaranteed in a happy not-so-little circle of debt. Carvana always repays the short term floorplan with the back end GPU, and lenders line up to fuel CVNA with the money they need to buy more cars.

And it’s important to mention: that cash pool is barely tapped. They have $2+ billion cash they can unlock just by increasing their balance sheet.

Back to the beginning. I think we have established that Carvana can pay for the bulk of its short term debt due in 2022, but remember there is still about $600 million that they will still have to cover, mostly for real estate expenses. I think they can swing it… check out the total cash on hand. This includes restricted cash from the short term loans.

Since there won’t be any additional debt incurred from the ADESA deal for years, it is safe to assume Carvana will double (or more) their cash on hand based on prior year trends. These aren’t big cash jumps for a company valued at over $25 billion, but even without restricted cash I expect Carvana will have at least $600 million in free cash to pay down debt, and perhaps restructure the rest if they can’t quite get there.

Let’s do one final recap. Carvana borrows cash to buy cars so it can originate loans on 80% of their sales. That credit is effectively unlimited because it is collateralized on growing inventory and accounts receivable, and the balance sheet always goes up with the Ally guarantee and their regular amendments. Most of the big debt is postponed for years, including the ADESA purchase, so I think they will skate through 2022 without a raise or a bankruptcy. The long term debt bubble, though, that’s a whole different story.

And what about ADESA? What’s the point? Buying and selling thousands of cars a week certainly takes up a lot of space, so I think this is very much a logistics based decision for Carvana. The company has struggled painfully with title and registration issues as well, to the point of illegality. Since it does not have a dealer license in every state, ADESA offices handily come with a staff of title clerks and dealer licenses. Although they seem to have drastically overpaid, I don’t think they have any other options if they want to acquire vehicles at a faster rate.

The thing is, I don’t think they’ll be acquiring them by shipping out flatbeds to people’s homes and picking up vehicles anymore. That gets expensive. So does owning or leasing vehicle reconditioning centers (side note, much of their real estate such as their vehicle improvement centers is leased through their parent co, DriveTime).

Furthermore, the business case for ADESA looks much worse for Carvana than it did under KAR because of the likelihood of current consignors (Carvana’s competing dealers) looking elsewhere to sell their fresh trades. Who would want their competitor scalping all the best trade-ins? Carvana would love that, but many dealers will flock to Manheim. Instead Carvana most likely plans to use the ADESA network (and their extra $1 billion for refurbishment) to become “evaluation centers” for regular people who want to sell their cars. Sure, Carvana will still make an online offer, but now customers will have to drive to an ex-ADESA location to pick up their check, and this only after a mechanic checks out the car. Sound familiar? That is the Carmax business model. And it works. Carmax also owns an internal auction, and sells to other dealers, but it's not one of the largest auctions in the country like ADESA is, because of course, Carmax keeps the good stuff for itself.

If you liked this piece, please feel free to comment and let me know. Your feedback is greatly appreciated!