Mullen Auto - Has Anyone Done Due Diligence?

Mullen Auto - Has Anyone Done Due Diligence?

In recent weeks, Mullen Technologies (MULN) has landed blow after blow to shorts, at one point ripping 500% higher in a month (low of $0.61 2/22/22, high $3.31, 3/22/22). The interest and volume surge has come in large part from retail traders, some of whom believe they have stumbled on the next Tesla, while others believe the company is being set up to fail by hedge funds and market makers.

*Author’s note - this report was completed week of March 28th and was pending review. The release of the Hindenburg Research short report published today, April 6th, which validates many of the findings below, has expedited my release.*

These communal attempts to “squeeze the hedgies” tend to ring with a tone of indignation about market manipulation, but looking deeper into this company reveals a much uglier story that leads me to believe that Mullen is perfectly capable of failing all by itself, despite their new “strengthened balance sheet” claim. Investing in this company should give pause to any investor who thinks about the ethics of their trades.

A Little Backstory

Mullen began in 2012 with David Michery purchasing Mullen Motors, the multi-rooftop used car dealership group that once marketed, but never sold, a sports car called the Mullen GT. Until then, Michery was a music producer/record label owner representing rapper Nate Dogg, who passed away the year before in 2011. Their biggest hit “Regulate” may be appropo listening, considering the dealings of his new company.

While it isn’t clear what prompted him to switch to the automotive industry with no prior experience, it’s possible that California-based Michery saw the burgeoning electric vehicle scene and decided to make his own. By 2014 he bought the technological remnants out of bankruptcy for the defunct and depressing Coda EV sedan (itself a “glider” chassis based on a 1990’s Mitsubishi, reworked by a Chinese automaker) and remarketed briefly as the Mullen 700e - perhaps with the intention of retailing them through the Mullen dealerships. It is unclear if any cars were ever sold, but Mullen still has several Codas sitting at their various facilities.

The company then rebranded to Mullen Technologies, and acquired a few other attempts to make money, including a 3rd party vehicle listing site, an auto loan resale business, and even an “energy” company which purportedly used the Coda facility to produce ventilators during COVID19. None of these ventures, including the dealership (which may have been spun off prior to SPAC, along with the loan securitization business) show any revenues in their filings today after merging with Net Element (NETE). Mullen’s new focus is forward looking, and is all about the Mullen FIVE, and less prominently, the Dragonfly sports car.

Car Talk

Let’s dig into the cars before we talk finances: Mullen does not build cars. The Dragonfly is simply a rebranded Qiantu K50 - they didn’t even bother to change the logo on the car. It’s been touted by the company since 2018, but has proven difficult to import to the US. This YouTuber documents his ordeal attempting to buy a K50 to drive on US roads and the company finally shipped him what he called “a pink golf cart” instead. This ordeal is both sad and funny from multiple angles, and even though the Mullen reservation page is still open to reserve a Dragonfly, the 10Q revealed that Mullen still has no agreement with Qiantu to bring this car to the US.

On to the FIVE. This is where Mullen puts their major attention, and the show cars received praise at the LA Autoshow in November 2021, which launched the company into prominence at around the time their SPAC deal was completed. It’s important to remember that the two existing FIVEs are just show cars. According to this journalist, Michery told him they cost $1.5 million each to build. The 10Q also speaks to over $2 million in contract payments to companies who built the concept cars.

No Such Thing as Bad News?

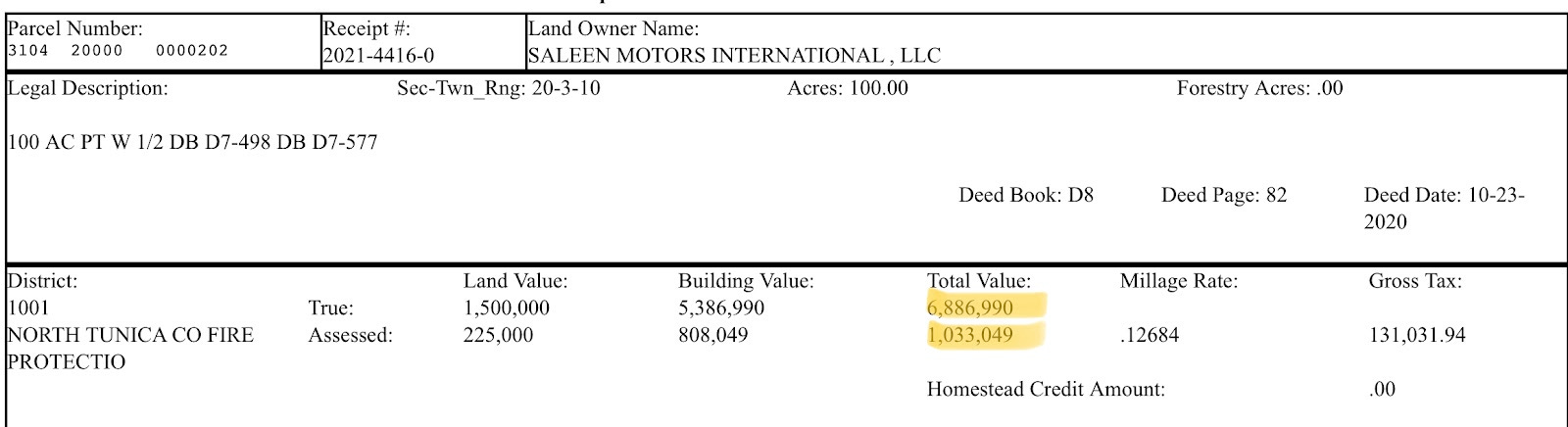

So where does Mullen want to build the FIVE? On Nov 15th, 2021 the company closed on a 124,000sf manufacturing facility in Robinsonville, Mississippi at 1 GreenTech Drive. According to the transaction record, Mullen purchased this property for $12 million from Saleen Automotive, which filed bankruptcy in 2018 along with its GreenTech Automotive partner who last used the facility. I looked up the tax card on the property and the current assessment is only about $1 million, with a “true value” listed of $6.9 million.

Certainly a good tax deal, but this seems like a major overpayment unless the factory came with a fully built out assembly system… unfortunately, that doesn’t seem to be the case. If we can judge by Mullen’s own photos and videos of the interior of the facility, it looks equipped with an overhead transfer lift or two, some nice lighting, and a couple of two post lifts. Besides the transfer lift, the equipment is on par with your neighborhood mechanic garage. It’s not vacant, but there is no automated assembly line, robotics, paint shop, or tools in this “Advanced Manufacturing and Engineering Center (AMEC)” and will need to be completely re-engineered for line production, or otherwise just build a few cars at a time. The company has signed a deal with Comau for the intensive work that needs to be done onsite for the retooling, which will be expensive. Their claimed “1.2 million sf factory expansion and test track” plans are nothing but a dream at the moment.

What about IP? There has been a lot of talk about Mullen’s solid state battery technology, including an announcement on February 28th which they claimed they would be using solid state cell technology from 2025 onwards. This announcement boosted the share price over 150%. I think the company has been misleading investors about this for two reasons. First, the 10Q notes their breach of contract over failure to co-develop solid state technology with a Chinese company called Linghang Boao, which indicates Mullen does not have their own battery tech. The deal has cost Mullen $390,000 so far, out of a total $2.2 million commitment that they don’t intend to repay due to Covid-related force majeur. Second, the replacement battery partner Mullen has selected for the FIVE is Nextech, a company indeed pursuing solid-state technology as well as Lithium Sulfur batteries, however neither technology is commercially available at this time. When they are (it looks good for Li-S tech), Nextech would sell this to any OEM that wanted it, not just Mullen. So this feels like a concerning lack of proprietary tech.

It appears that all of the innovation around the FIVE is actually limited to agreements similar to their partnership with Hofer powertrains, whose drive systems are clearly available off the shelf for any interested clients. There are a few small milestones at least. The company has released agreements with ARRK for engineering the actual vehicle, Durr for factory production systems, and DSA for diagnostics. Really, these partnerships should remind readers that nobody actually working at Mullen has any experience designing or engineering vehicles.

Financial Situation

This rollout sounds really expensive. How much can Mullen afford right now? Looking at their financials, R&D spending so far is almost exclusively the development of show cars. The company is already struggling to pay back the mountains of debt it has accumulated through its pre-SPAC entity, Net Element (NETE), and new debt it continues to add on. Current balance sheet liabilities show over $19,000,000 due of the current portion of convertible notes ($23,192,500 total debt of convertible notes), of which $3.7 million is already in default bearing 15% interest.

An additional $14 million matures in 2022 bearing a staggering 28% interest. Direct from the 10Q, “for the three months ended December 31, 2021 and 2020, we recorded interest expense of $22,438,945 and $2,406,330, respectively.” (Emphasis mine). Really, for three months?? It seems a substantial portion of this debt is due to Drawbridge Capital, which has accrued over $11 million in interest on their remaining $14 million principal. Their loans are also currently in default, and Drawbridge has entered a repayment agreement with the company and restructured the debt through a stock sale. More on stock sales in a moment, unfortunately we are not done yet.

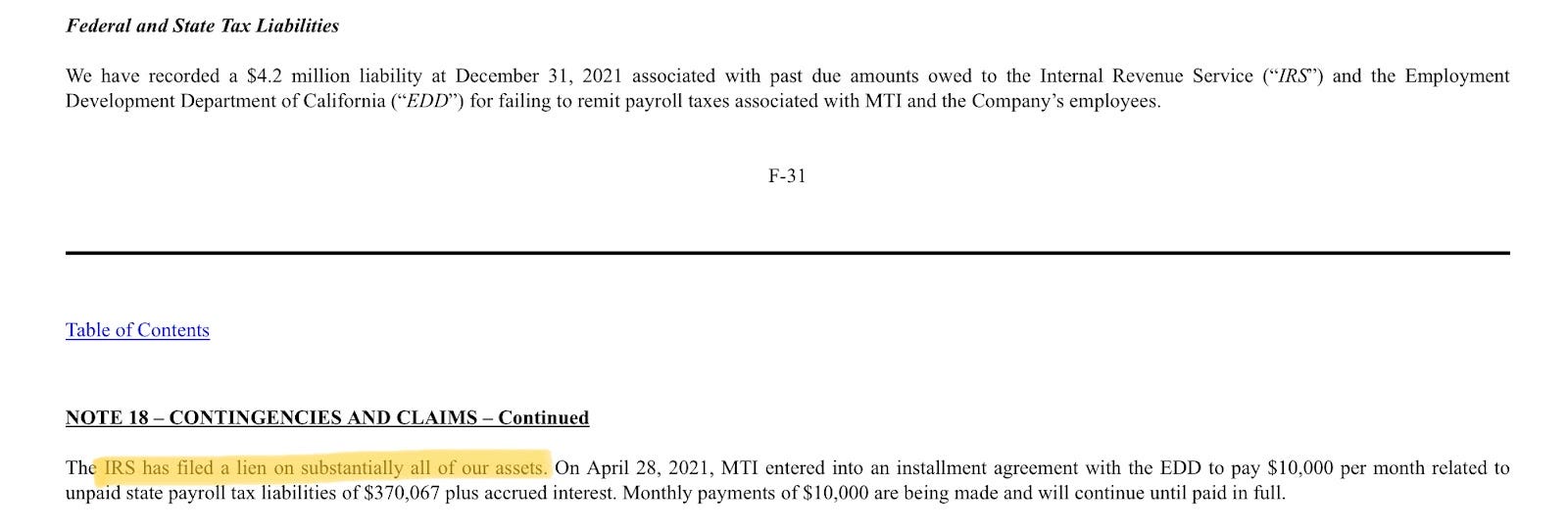

The debt discussed above does not include an additional $19 million in accrued expenses, which includes delinquencies to IRS. The IRS currently has a lien on all company assets and Mullen is forced to make $10k/month payments on an existing unpaid $370,000 unpaid tax liability. It gets worse. The 10Q states “delinquent IRS and state tax liabilities as of December 31, 2021 and September 30, 2021 are $4,277,297 and $3,904,720, respectively.” That is going to cost a lot more than $10,000 per month.

In addition, there are/have been other liabilities that may turn into lawsuits, and if the past is any indication, the judgements will not be in their favor. Mullen’s prior entity before the SPAC merger lost a suit with IBM for $5.6 million that Mullen is paying for, and there is still a risk of litigation with violations of contracts with Raymond James over failure to deliver proceeds generated from the SPAC merger, and the noted breach of contract with Linghang Boao.

Let’s now take a look at assets, and see if there’s anything they can use as collateral.

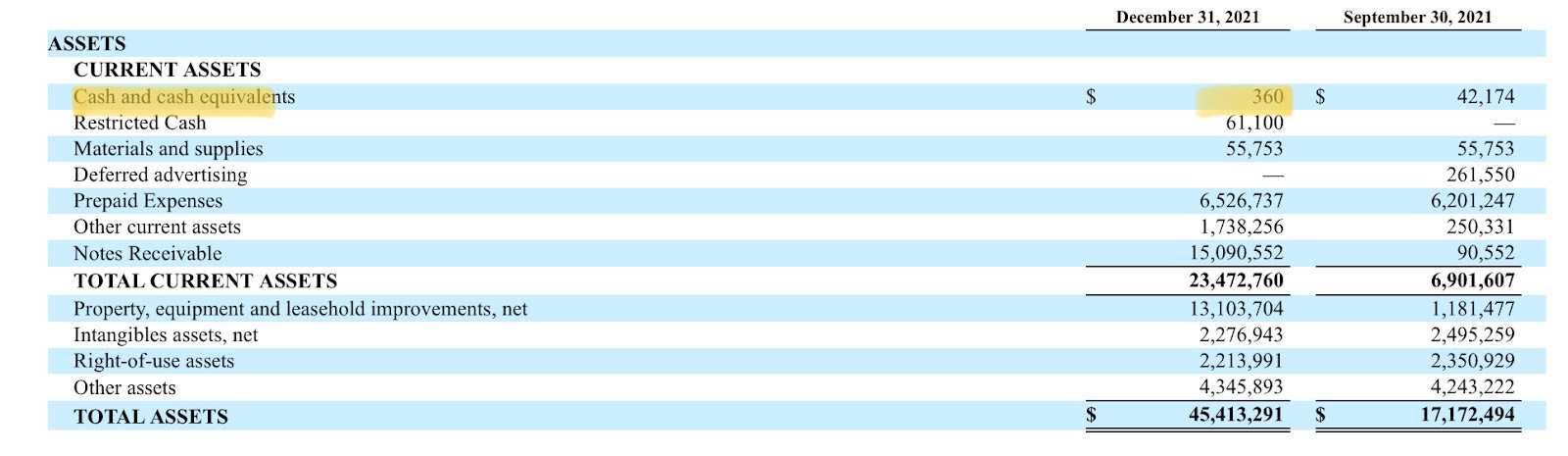

The company has a total cash balance of $360 (no that’s not missing any zeros) as of Dec 31st, 2021, and has been taking loans from its own employees, including Michery and board member Mark Betor. To be fair, the loan had very attractive terms: $1,000,000 with a 90 day 15% repayment guarantee. There’s clearly a plan in place to get some liquidity… so let's dive deeper.

As I mentioned earlier, it seems any revenue that could be generated from the dealership group and loan securitizing business is outside of the publicly traded Mullen Technologies company, even though there are still about 60 vehicles for sale online at Mullen-branded dealerships. Is there anything else they can sell, or anywhere else at all the money could come from?

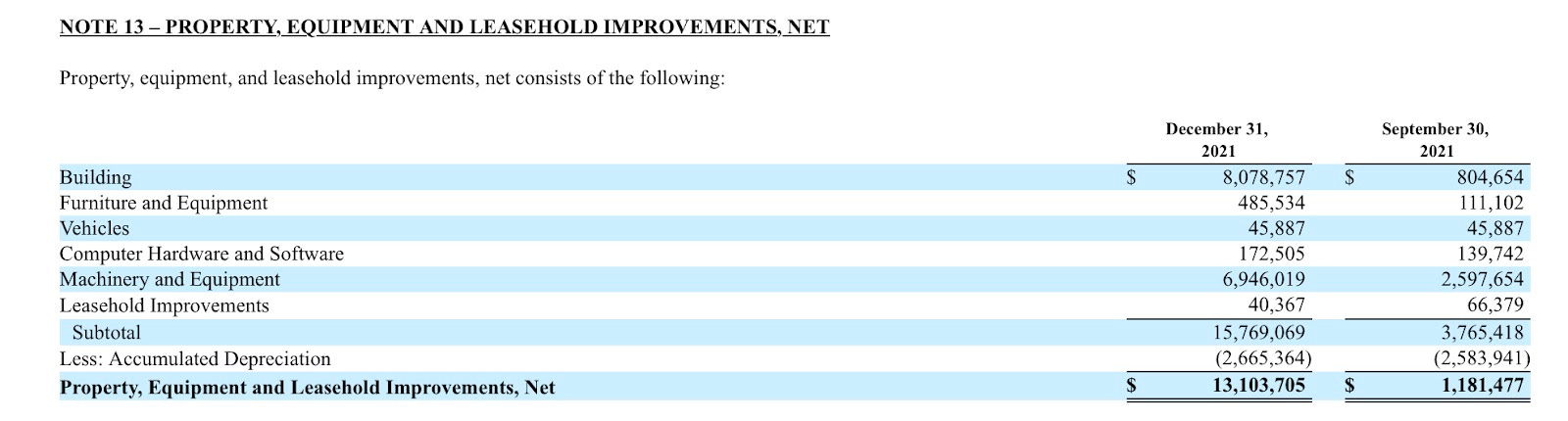

Taking another look at the balance sheet, the $12 million factory purchase has made its way on, adding roughly $8 million since Q3 (property list below).

The $4 million in “other assets” seem mostly to consist of the leftover Coda vehicles, which are effectively unsaleable, a Qiantu K50, and the two concept FIVEs, which have already served their purpose for marketing. So this seems quite generous, but there are other places to investigate.

Down the Rabbit Hole

Looking at accounts receivable, I was surprised to see that a previous article praising the company’s growth potential found no risk underlying their $15 million equity agreement with a company called CEOCast. This seems to be a promise to pay down debt that Mullen took over from NETE, to a legacy debtor RBL capital. But it would certainly be great for the balance sheet if they had more cash coming in this way…

Sourced from 10Q

And there seems to be. A company called ESOUSA holdings which is one of Mullen’s largest shareholders indeed committed an additional $30 million in equity. Unfortunately, it begins to get complicated. This financing arrangement is very creative and before we explore it, we need to understand who is behind it.

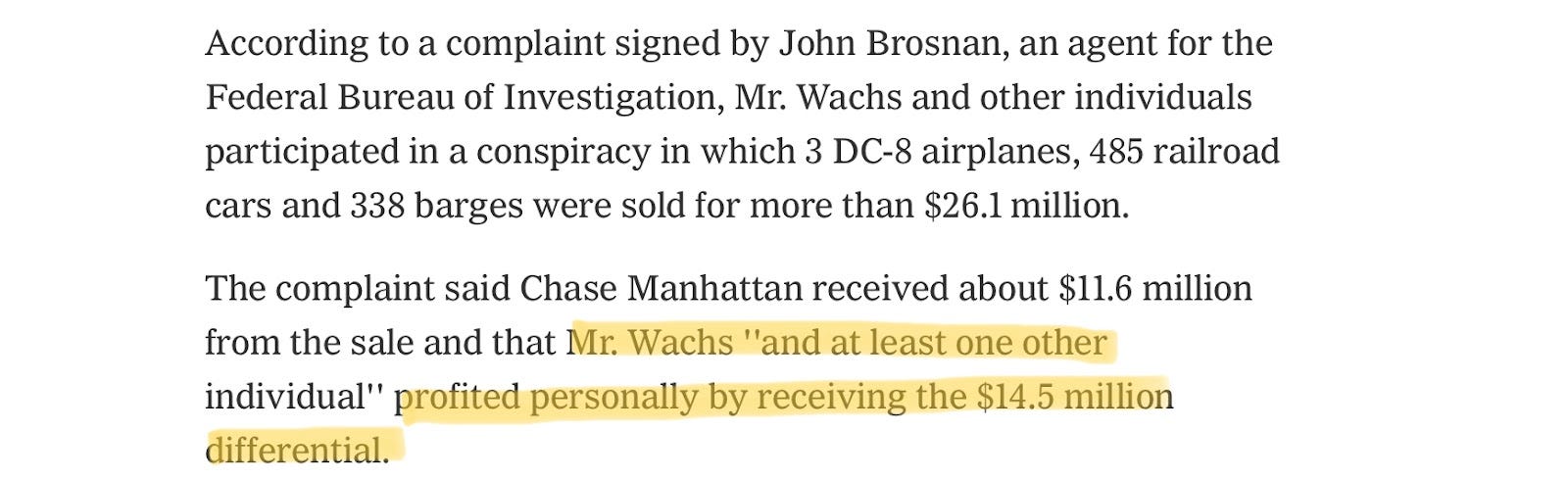

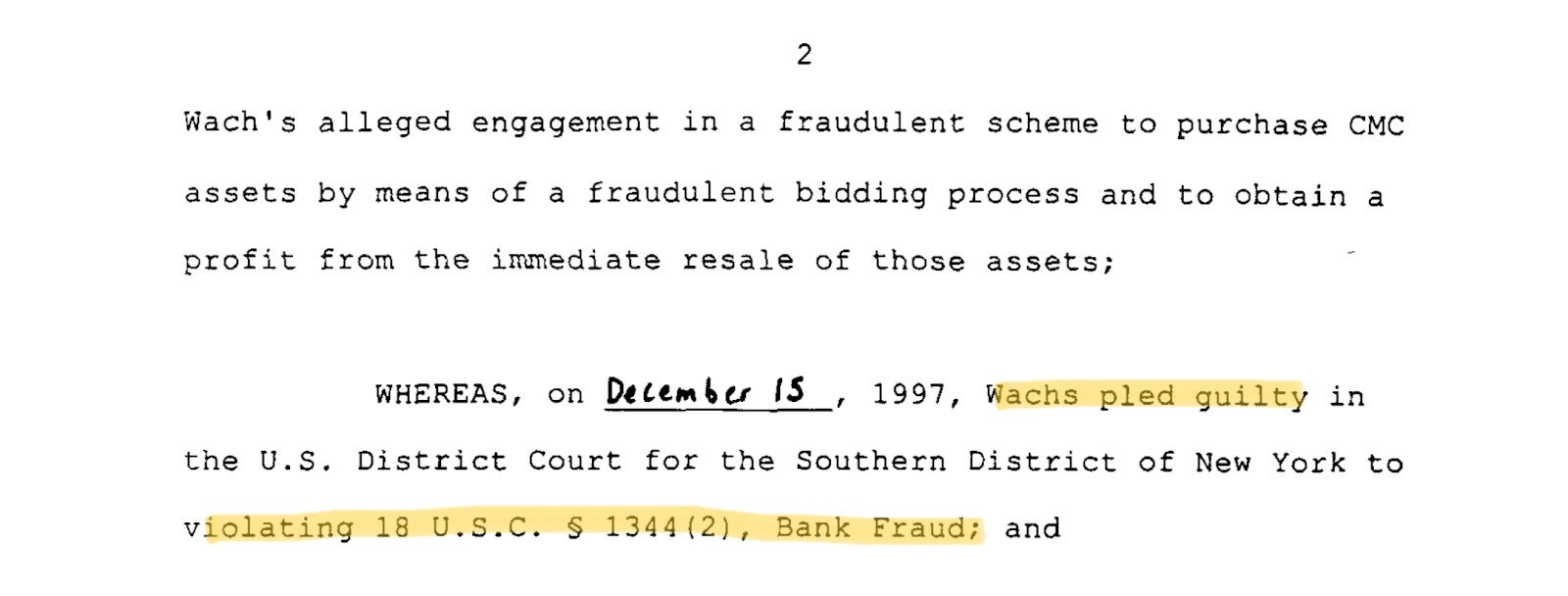

ESOUSA plays an outsized role in this story. Through nearly every SEC filing submitted by Mullen, the company name ESOUSA Holdings is referenced. This company is run by a man named Michael Wachs, who in 1997 was banned from the banking and brokerage industries and went to jail for embezzling millions of dollars while he was an executive at Chase Manhattan.

From the NY Times in 1996, details of the charges:

And guilty plea:

Before the Mullen SPAC merger with Net Element (NETE), ESOUSA was a large NETE investor, but at the time it seemed he was running the company under his wife’s name, presumably to avoid attention. The cited Wall Street Journal article shows how Wachs covered his identity for years, but now he is directly named in Mullen’s S-3 prospectus as the man behind CEOCast and ESOUSA.

Sourced from Feb S-3 share issuance prospectus

On February 3rd, 2022 Mullen filed and received approval for a shelf offering to issue 228 million shares comprised almost entirely of insider warrant exercises and conversion of preferred shares. Right there, plain as day, the underwriter for the share issuance is listed as “ESOUSA Holdings LLC” (source SEC S-3).

Now I can’t dive into the legal pool here. I don’t know whether an underwriter for a secondary offering is subject to the same scrutiny as those involved at an IPO, but wouldn’t the underwriter for any stock sale fit the definition of a “broker/dealer?” How close or over the line is this for someone who has been expressly denied permission from performing such roles by a US District Court and the Board of Directors of the Federal Reserve?

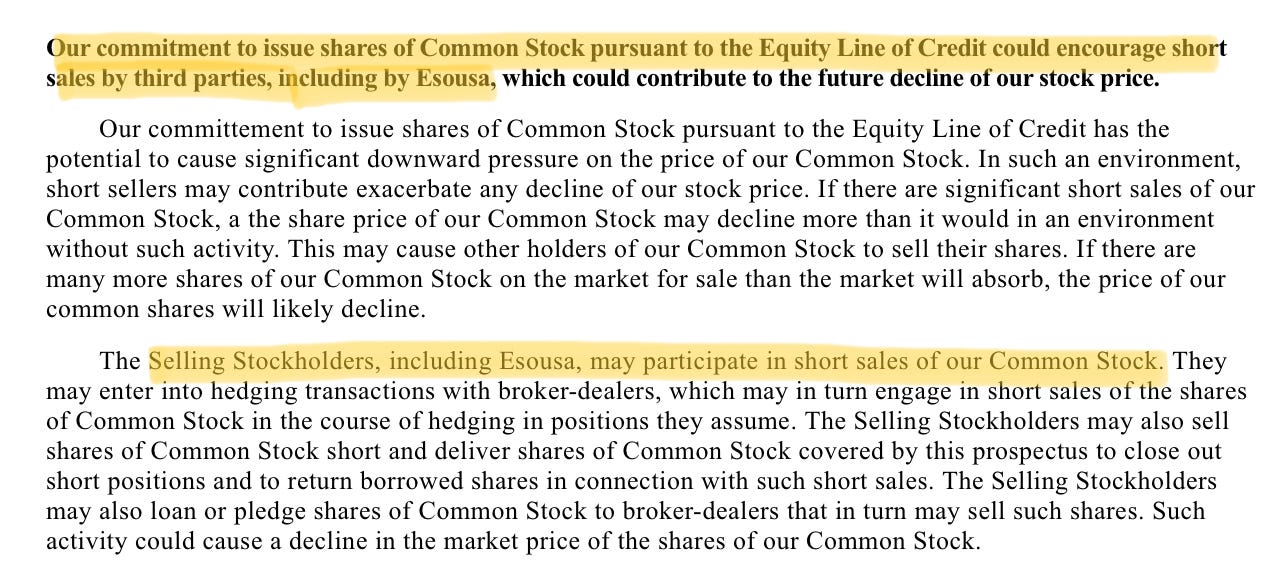

Another prospectus was just released March 28th offering an additional 253 million shares and all references to ESOUSA as underwriter have been replaced with this:

There must have been a big enticement or a big mistake to risk this association publicly. Mullen’s complex arrangement of warrant sales and corporate financing may explain why.

If The Juice Ain’t Worth the Squeeze…

Remember the $30 million equity line mentioned earlier? This deal essentially gives Wachs a 30% share discount with almost no lockup period, if I’m interpreting correctly.

The formula involves buying an overinflated number of shares at a below market rate per each draw down, which if I’m not mistaken, he can immediately turn around and sell at the market price ten days after purchase. For financial and legal experts reading, is this a license to print insider money? Even if it is being used to pay off debt, is that arrangement legal? Or is there another explanation for this?

As convoluted and hard to follow as the company is, the underwriter is the one company (individual, in this case) who would know every detail, especially the exact date and time of dilutive share issuances from the shelf offering. This could potentially allow him to strategically short with leverage through put options, amplifying profits on the company’s downwards share price right before the common stock periodically floods the market. Perhaps that’s why this was disclosed in the S-3?

Going even further, back in 2017 when Net Element was still NETE and Mullen was still private, ESOUSA was granted 404,676 5-year warrants with an exercise at $11.12, which expire year-end 2022. These would have carried over in the new company (MULN), but at a market price well below the strike, these warrants would be completely underwater. According to the 10K, ESOUSA and Mullen worked a deal just before the merger to reduce the strike price to $6.79, perhaps with the hope the share price could rise enough to cover. Wachs would still have the potential to cash out big if the company could pump above that point, while improving his margin on discounted shares. Could the determined short squeezers have accidentally and unknowingly been helping to enrich a conman?

Where Are Things Now?

Quite the ball of yarn to unravel to get here and I’m sure there is more I’m missing. Just to recap so far, a convicted embezzler is the company’s only source of new equity, and in exchange he is allowed to acquire shares at a discount, immediately sell for profit, and then short sell on the expected effects of his own dilution as the corporate underwriter. That seems… creative. There must be some other words for it…

So how much shorting is really happening? Is the MULN Army right? The short interest as percent of float seems high, at 40% according to TD Ameritrade as of 3/15, but currently TD publishes only 35 million shares outstanding, which was valid through February according to the company’s 10Q. But I really wonder, how can anyone know in this case what percentage of shares are being held short and by who?

Supposedly, zero shares are available to short as of late, so the borrow is completely tied up, however with the many occasions shares have increased (first before SPAC, revised after SPAC, warrants exercised, plus two new public issuances), it seems that honest float and outstanding share numbers have simply not caught up to publication yet, making published short percentages meaningless.

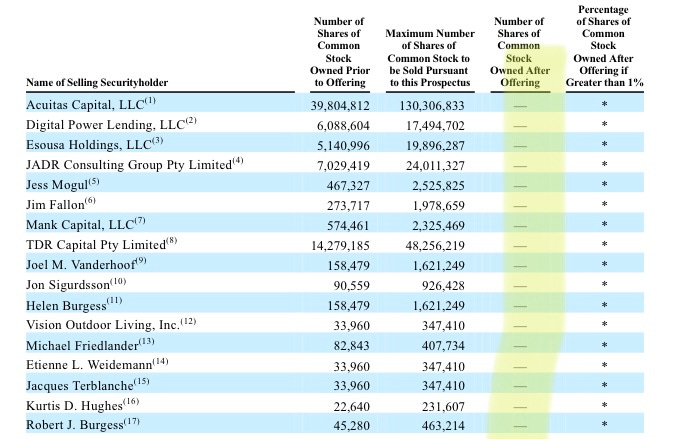

Ok, obviously it’s not all completely pointless, but it is worth remembering that between the two latest prospectuses on Feb 3rd and March 28th, over 490 million shares have been authorized to convert to common stock. Below is the note in the newest prospectus for 253 million shares which indicates there are already 239 million shares outstanding as of March 25th, so these moving goalposts are completely distorting the assumptions people are making based on free float.

A Walk to the Exit

Most investors seem to want to get out completely this time around. In both share issuances, inside investors began selling warrants and preferred shares, leaving them with large amounts of common stock. Because the shelf offering permits the underwriter to drip shares onto the market, rather than dumping them all at once, it is up to ESOUSA and other insider shareholders to determine when exactly to sell to outside investors and close out their position.

The company in total stands to gain over $100 million if all warrants were exercised, and certainly many investors will do that as they exit their positions. I expect to see some of the cash from warrant exercises like these below to also show up as cash on the latest balance sheet for their Q1 earnings, and more throughout the year. At the time of this writing, Mullen announced a $60 million strengthened balance sheet for Q1, and this is just a portion of how they have done that.

Who Does This?

It’s all very eye-watering. All I know for sure is that the cast of characters in the MULN saga is filled with interesting backstories. Net Element (previously NETE) merged with MULN as a SPAC deal last November, and prior to that point NETE never turned a profit during its ten year run as a public company. The group was run by Oleg Firer, a Russian billionaire with deep connections to Putin. Oleg was accused of siphoning American money to Moscow and operating as a Moscow intelligence asset, and known for conducting scams involving young women in Miami (paywall). While Firer is no longer beneficially involved in MULN, he did receive a 15% stake at the merger and may still hold a small position, but more importantly, a couple of his executives and investors stuck around.

Long serving Chief Legal Officer of Net Element Steven Wolber remains the Chief Legal Officer at Mullen, and sold millions of dollars of his NETE stock options last year. Mullen’s CFO Jerry Alban was the COO at Net Element. Jonathan New, who was CFO at Net Element, is on MULN’s board and worked with Russian billionaire and financier Mike Zoi, who was one of the two largest investors at NETE. The other was Kenes Rakishev, a relative of Kazakh president with known Kremlin allegiances and business dealings in Moscow. It seems NETE’s major financiers mostly cashed out upon the merger, although once again, due to the major fluctuations on authorized shares and shares outstanding, it is hard to find accurate and up to date information on the true holdings of any major investors today. It may be worth keeping all of these names in mind for future reference.

Lessons Learned

Ultimately, what this story comes down to is that due diligence is important. This shockingly deceptive company should not get the benefit of good PR and retail trader endorsement, and ideally should be shorted to zero before ESOUSA can get his hands on even more shares by underwriting the shelf offerings. The terms of his equity agreement state he is not obliged to buy stock if the price is under $3.00/share. The reason for this? The returns diminish the lower the price goes. Retail investors buying up the issuance only helps ESOUSA expand his profit margin when he sells shares for himself and other insiders, and then inadvertently gives him more public float to borrow against to perfectly time a short position against the next offering.

Frustrated traders who see massive trading volume in small cap companies may think by buying the stock they are teaching evil shorting hedge funds a lesson. Some have even shown sympathy towards CEO and majority owner Michery, alleging that he is the victim of a short and distort scheme (unfortunately I can no longer find this tweet). But for those traders who feel it is their moral duty to squeeze hedge funds and to “crush the shorts,” they may in fact be helping much worse people. Sometimes betting that bad companies will make bad decisions is the right thing to do.